A roof repair or replacement can cost anywhere from $5,000 to $25,000 or more, and most homeowners do not have that sitting in savings. That is exactly why understanding your roofing financing options as a homeowner matters so much. The right financing plan can mean the difference between fixing a failing roof now and waiting until minor damage becomes a structural emergency. This guide walks you through every major option available in 2026, from government-backed loans to contractor financing, so you can make a confident, informed decision.

Table of Contents

Key takeaways

| Point | Details |

|---|---|

| Know your credit before applying | Your credit score directly affects which loans you qualify for and what interest rate you will pay. |

| HELOCs offer the lowest rates | HELOC APRs typically run 7% to 9%, making them the most affordable option for homeowners with equity. |

| Government programs exist for many | FHA Title I and USDA Section 504 loans serve homeowners who lack equity or have limited income. |

| Deferred-interest plans carry risk | If you do not pay off the balance before the promotional period ends, interest accrues retroactively from day one. |

| Contractor financing speeds things up | Point-of-sale financing through your contractor can approve loans up to $100,000 and get your project started faster. |

What homeowners need to know before seeking roofing financing

Before you apply for any loan or financing plan, you need a clear picture of where you stand financially. Skipping this step leads to surprises, and surprises in financing are rarely good.

Your credit score sets the foundation. Lenders use your credit score to determine whether you qualify and at what rate. A score above 700 opens most doors. A score below 620 may limit you to personal loans with higher interest rates or specific government programs. Pull your free credit report before you start shopping so you know exactly what you are working with.

Home equity changes your options significantly. If you have owned your home for several years and built up equity, you may qualify for a Home Equity Line of Credit (HELOC) or a home equity loan. Both use your home as collateral, which is why lenders offer lower rates. If you have little to no equity, these options are off the table and you will need to look at personal loans, credit cards, or government programs instead.

Here are the key financial factors to review before applying:

-

Credit score: Aim for 700 or higher for the best rates. Check all three major bureaus.

-

Home equity: Calculate your current home value minus your remaining mortgage balance.

-

Debt-to-income ratio: Most lenders want this below 43%. Add up your monthly debts and divide by gross monthly income.

-

Monthly budget: Determine the maximum monthly payment you can comfortably handle before comparing loan terms.

-

Documentation: Gather pay stubs, tax returns, mortgage statements, and a roofing estimate before applying.

Pro Tip: Get a written estimate from your roofing contractor before approaching any lender. Having a specific dollar amount makes your application stronger and prevents you from borrowing more or less than you actually need.

Interest rates vary widely depending on the product you choose. HELOC APRs typically run 7% to 9%, while personal loans range from 12% to 30% and credit cards can hit 25% to 35%. Knowing these ranges before you apply helps you set realistic expectations and compare offers fairly.

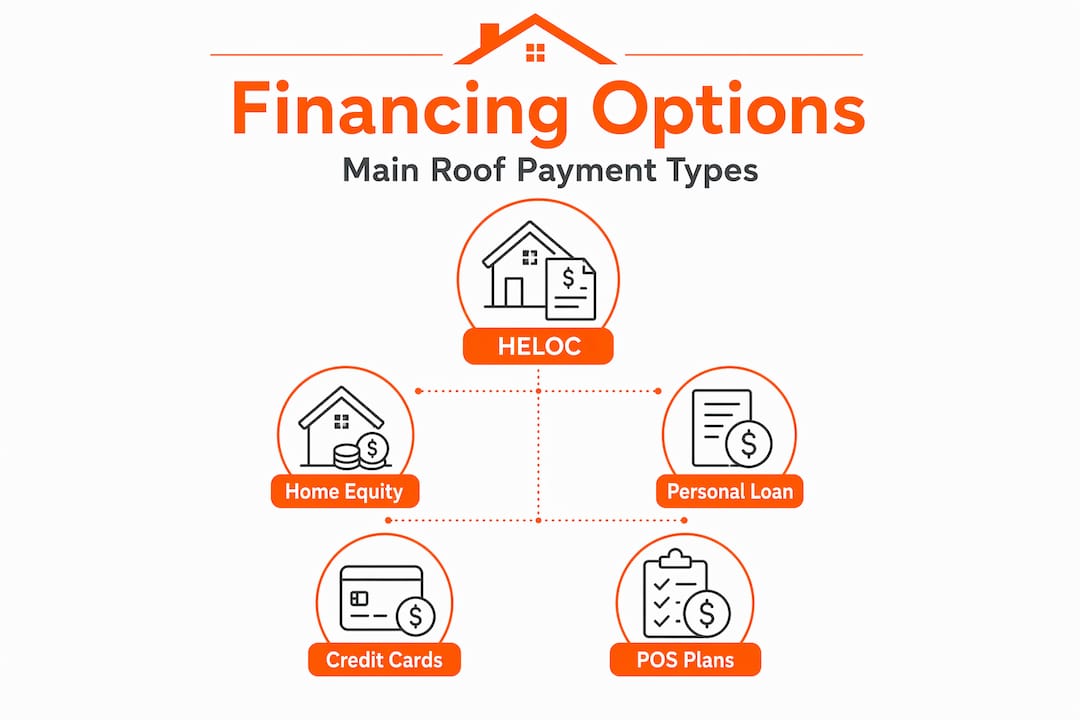

Top financing options for roof replacement and repair

Understanding how roofing financing works starts with knowing what products are actually available. Common payment options include cash, credit cards, HELOCs, personal loans, deferred-interest plans, and contractor financing. Each one suits a different financial situation.

Home equity line of credit (HELOC)

A HELOC gives you access to a revolving credit line secured by your home’s equity. You draw funds as needed during a set period, typically 5 to 10 years, then repay the balance. Average national HELOC rates sit around 7.17%, making this the most affordable option for homeowners who qualify. The catch is that rates are variable, meaning your payment can increase if market rates rise. There is also a real risk: your home is the collateral, so missed payments have serious consequences.

Home equity loan

A home equity loan gives you a lump sum at a fixed interest rate, with home equity loan rates averaging 7.85% to 7.99%. Payments are predictable month to month, which many homeowners prefer. This option works well when you know the exact cost of your roof replacement and want payment stability over time. The same collateral risk applies here as with a HELOC.

Personal loans

Personal loans do not require home equity, which makes them accessible to more homeowners. Approval is typically faster than equity-based products. The tradeoff is cost. Rates run significantly higher, from 12% to 30% depending on your credit profile. For smaller repairs in the $3,000 to $8,000 range, a personal loan can be a practical and fast solution.

Credit cards

Credit cards are convenient but expensive for large roofing jobs. They work best for minor repairs you can pay off within one or two billing cycles. Using a card with a 0% introductory APR offer is one way to manage a smaller project without interest, provided you pay it off before the promotional period ends.

Deferred-interest and same-as-cash plans

These plans advertise 0% interest for a promotional period, typically 3 to 12 months. They sound attractive, but the fine print matters. If you do not pay the full balance before the promo expires, interest accrues retroactively from the original purchase date. That can add hundreds or thousands of dollars to your total cost overnight.

Government-backed programs

Two programs stand out for homeowners who lack equity or have limited income:

-

FHA Title I loans: Up to $25,000 for single-unit homes with fixed interest rates and terms up to 20 years. No significant equity required. Backed by the U.S. Department of Housing and Urban Development.

-

USDA Section 504 Home Repair: Available to low-income rural homeowners. Offers fixed 1% interest loans up to $40,000 repayable over 20 years. Grants are also available for seniors. Eligibility depends on income level and property location.

These government roofing grants and loan programs are underutilized. Many homeowners simply do not know they exist.

Contractor point-of-sale financing

Many roofing contractors now offer financing directly through third-party platforms integrated into their quoting process. These platforms can approve loans up to $100,000, and the application happens right alongside your estimate. This approach speeds approvals and removes friction from the process.

| Financing option | Typical APR | Requires equity? | Fixed or variable | Best for |

|---|---|---|---|---|

| HELOC | 7%–9% | Yes | Variable | Large projects, flexible draw |

| Home equity loan | 7.85%–7.99% | Yes | Fixed | Full replacement, stable payments |

| Personal loan | 12%–30% | No | Fixed | Mid-size repairs, no equity |

| Credit card | 25%–35% | No | Variable | Small repairs, short payoff |

| FHA Title I | Fixed, HUD-set | No | Fixed | Low-equity homeowners |

| USDA Section 504 | 1% fixed | No | Fixed | Rural, low-income homeowners |

| Contractor financing | Varies | No | Fixed or variable | Fast approval, large projects |

Pro Tip: Ask your contractor whether they offer point-of-sale financing before you seek outside loans. The application is simpler, the approval can be faster, and you may find better terms than you expected.

How to choose and apply for roofing financing

Knowing your options is one thing. Getting through the application process confidently is another. Follow these steps to move from estimate to approval without unnecessary stress.

-

Assess the urgency of your roof repair. A minor leak and a roof with structural failure require very different timelines. If your home is at risk, you need a financing option that approves quickly, such as a personal loan or contractor financing.

-

Get a detailed written estimate. Before you apply anywhere, have a licensed contractor inspect your roof and provide a written cost breakdown. This document is required by most lenders and prevents you from guessing at loan amounts.

-

Check your credit score and pull your report. Look for errors and dispute any inaccuracies before applying. Even a small score improvement can lower your interest rate meaningfully.

-

Compare at least three loan offers. Do not accept the first offer you receive. Compare APR, loan term, monthly payment, and any fees. A lower monthly payment is not always the better deal if it comes with a longer term and more total interest paid.

-

Read every line of the fine print. Pay special attention to prepayment penalties, variable rate caps, and promotional period expiration dates. These details determine your actual cost.

-

Consider your contractor’s financing program. Financing integrated into contractor proposals reduces delays and gives you a clear picture of total project cost alongside payment options. Ask about it during your estimate appointment.

-

Submit your application with complete documentation. Incomplete applications slow everything down. Have your income verification, tax returns, mortgage statement, and roofing estimate ready before you click submit.

-

Plan your repayment from day one. Set up automatic payments if possible. Know your payoff date for any promotional plan. Budget for the monthly payment before the project even begins.

Pro Tip: If you are considering a HELOC, understand how the draw period works. Draw periods can end abruptly, causing your monthly payment to jump significantly when the repayment phase begins. Plan for that transition in your budget.

Common mistakes to avoid when financing your roof

Even homeowners who do their research make avoidable mistakes. These are the ones that cost the most.

-

Ignoring deferred-interest terms. Many homeowners assume same-as-cash means no interest regardless of what happens. It does not. Retroactive interest on deferred plans can dramatically increase your actual cost if you miss the payoff deadline by even one day.

-

Underestimating total loan cost. A $15,000 roof at 18% APR over five years costs you over $22,000 total. Always calculate total repayment, not just monthly payments, before committing.

-

Putting a large job on a credit card without a payoff plan. Credit cards are not designed for multi-thousand-dollar balances held over months. The interest compounds quickly and can trap you in a cycle that is hard to exit.

-

Using equity loans without confidence in repayment. Home equity loans and HELOCs carry collateral risk. If you miss payments, your home is at stake. Only use these products if you are genuinely confident in your ability to repay.

-

Skipping government programs without checking eligibility. Many homeowners assume they will not qualify for FHA Title I or USDA Section 504 programs without ever checking. FHA Title I offers a solid alternative for homeowners with low equity, and USDA programs serve rural areas specifically. A five-minute eligibility check could save you thousands.

-

Not asking your contractor about financing. Contractors who offer financing often have access to competitive rates and simplified applications. Skipping that conversation means you might be paying more than necessary through outside lenders.

“The most expensive financing mistake is not the one with the highest rate. It is the one you did not fully read before signing.”

My honest take on roofing financing

I have seen homeowners make smart financial decisions and costly ones when it comes to paying for roof work. What separates the two groups is almost always the same thing: how many questions they asked before signing anything.

In my experience, the homeowners who come out ahead are the ones who treat financing like part of the roofing project itself, not an afterthought. They get the estimate first. They check their credit. They compare at least two or three options before committing.

What I find genuinely underused are the government-backed programs. A lot of people assume they will not qualify, so they never apply. But if you are a rural homeowner with limited income, the USDA Section 504 program at 1% fixed interest is one of the best deals available anywhere in the home improvement financing space. FHA Title I is similarly overlooked by homeowners who have not built significant equity yet.

My caution around deferred-interest plans is real. I have seen homeowners get hit with retroactive interest charges because they missed the payoff date by a few weeks. The plan looked like a great deal on paper. In practice, it cost them more than a personal loan would have. Always ask the lender specifically what happens if you are one day late on the final payment.

Contractor financing, when done right, genuinely helps. It removes the gap between getting an estimate and starting the work. That speed matters when your roof is actively leaking. The key is working with a contractor who is transparent about the terms and does not pressure you toward a specific product.

My overall advice: take the time to understand what you are signing. The right financing plan makes a necessary roof repair affordable and manageable. The wrong one adds financial stress on top of an already stressful situation.

— Sean

How Frenchroofing makes financing easier for you

Paying for a roof repair or replacement does not have to mean draining your savings or delaying a project that protects your home. Frenchroofing offers flexible financing options for homeowners so you can move forward with confidence, regardless of your budget situation.

Whether you need a full roof replacement or a targeted roof repair, Frenchroofing walks you through financing during the estimate process. No guesswork, no pressure. The team is licensed, CertainTeed Certified, and committed to treating every home with the same care they would give their own. You can start with a free instant estimate online and get a clear picture of your project cost before you make any financing decisions. Frenchroofing serves the Greater Portland Metro area and surrounding communities, and the team is ready to help you find a path forward that fits your situation.

FAQ

What are the most affordable roofing financing options?

HELOCs and home equity loans typically offer the lowest rates, with APRs around 7% to 8%, but they require home equity. For homeowners without equity, FHA Title I loans and USDA Section 504 programs offer fixed, low-interest alternatives.

How does contractor point-of-sale financing work?

Contractor financing is offered directly through your roofing contractor using a third-party lending platform. You apply during the estimate process, and approvals can cover up to $100,000 with faster turnaround than traditional bank loans.

Can I finance a roof repair with bad credit?

Yes. Personal loans are available to borrowers with lower credit scores, though rates will be higher. Government programs like FHA Title I also have more flexible credit requirements than conventional loans.

What happens if I miss the deadline on a deferred-interest plan?

If you do not pay the full balance before the promotional period ends, interest accrues retroactively from the original purchase date. This can add a significant amount to your total cost, so treat the payoff deadline as a firm deadline.

Do I need equity in my home to get roofing financing?

No. Personal loans, FHA Title I loans, USDA Section 504 programs, and contractor financing do not require home equity. These options exist specifically for homeowners who have not yet built significant equity or who prefer not to use their home as collateral.